As the world is poised to return to normal after the kickoff of worldwide vaccination efforts, economies are buzzing, and are expected to soon pick-up steam and recuperate the losses that were incurred by the COVID-19 pandemic. Unprecedented governmental stimuli and unsatiated demand from impaired industries will likely pave the way for an economic upheaval that is sure to propel value and cyclical equities to levels higher than ever before. Although the recovery within the western hemisphere (EU & USA) is expected to be slow and steady (especially considering the current extension of lockdown measures) (Yahoo Finance , 2020), prospects for markets on the other side of the globe paint a different picture altogether. Due to controllable infection rates, a growing middle-class consumer base, and weaker foreign currencies, emerging markets are primed to enter a phase of strong economic expansion. Promises for higher returns in these markets will therefore draw more investors and money towards these regions, enabling even greater (potential) growth for corporations. What exactly are emerging markets, and how can your investments benefit from them?

The term “emerging markets” (from now on dubbed EM) refers to the economies of countries that are undergoing industrialization as they become more developed (Oxford Business Group, 2021), and therefore has characteristics of a developed market, but does not fully meet its standards. Think of standards such as average GDP per capita, or the ease of capital inflow. Below the EM classification also exists the subcaste “Frontier Market” (FM), which is developing but is too small, risky, or illiquid to be considered an emerging one. Although an EM can transform into one that is labeled as “developed”, there has been a set of distinct countries that has been labeled as emerging for quite some time. Although some markets can be labeled differently depending on the scale of measurement, the following group of countries appears on every single list: Brazil, China, India, Mexico, Morocco, Russia, South-Africa, Russia, and Turkey (image 1). From a historical perspective, these were countries that either gained sovereignty in a later stadium after having been a colony for multiple years or suffered past historical economic downturns due to mismanagement and conflicts. This, in turn, resulted in their economies lagging behind those in the west, which turned into a downward spiral, as these countries subsequently lagged in every other aspect of development as well.

Image 1: Map of Emerging & Frontier markets around the globe (highlighted areas)

Although much has changed for the better in EM’s over the past couple of decades, past performance of EM’s on equity markets leaves much to be desired. Over the past 10 years (2010–2019) the MSCI Emerging Markets Index had an annualized return of 3.7%, compared to 5.3% for the MSCI World ex USA Index, and 13.6% for the S&P 500 Index (Umland, 2020). During these years global stock markets experienced depression-like performance. The aftermath of the Global Financial Crisis was high debt and low growth and ineffective monetary policy despite huge money printing and zero interest rates. The policies of Central Banks only benefited stocks in the United States, where technology and innovation sectors benefited from low discount rates, and earnings were pumped up by tax cuts and stock buybacks. The rest of the world saw low earnings growth, declining multiples, and weak currencies. (The Emerging Market Investor, 2021). However, these periods of lackluster returns have also been offset by periods of excessive gains. In the previous decade (2000- 2010), EM’s outperformed the rest of the world and the S&P by close to 9.0% (Umland, 2020). Investing in these markets, therefore, bring with it increased volatility and a big deviation from performance in developed western markets.

Although the Covid-19 pandemic has struck worldwide economies hard, emerging markets are expected to rebound relatively well compared to western developed markets. Trade-dependent economies, like Korea and Taiwan, are already well into their recoveries. Meanwhile, China, the first to impose COVID-19 closures, has quickly regained ground, as consumption roars back. Morgan Stanley projects that its economy will expand 9% in 2021, before moderating toward 5.4% in 2022 (Morgan Stanley, 2020). The recovery in emerging markets equities that began in late March picked up steam in the fourth quarter thanks to COVID-19 vaccine breakthroughs and the US election outcome. This resulted in the MSCI Emerging Markets Index outperforming global developed markets equities in 2020 (Lazard Asset Management, 2021). Furthermore, the major central banks, except China, have shown no inclination to raise rates, and inflation is expected to remain low in emerging markets overall, paving the way for higher growth. The pandemic may be felt for years to come. For emerging markets economies, however, the pandemic is not expected to greatly alter the long-term trajectory for growth. Indeed, in its latest forecast, the IMF projected 6% growth for emerging markets and 3% for developed markets in 2021, with the growth gap only widening after that (Yahoo Finance , 2020).

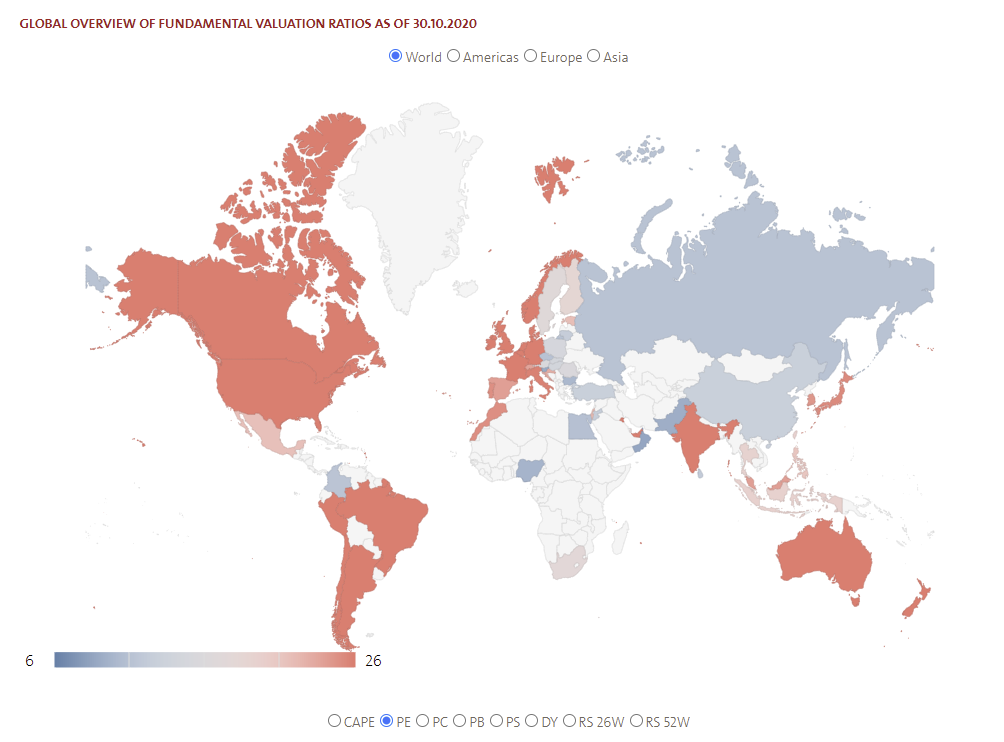

From a value perspective, investing in EM currently serves as an attractive option as valuations are relatively cheap compared to developed western markets. Image 2 shows a worldwide overview of P/E ratio valuations near the end of 2020, with Red indicating overvalued, and Blue indicating undervalued. It can be seen that much of the emerging markets fall into the grey / blue area, as opposed to the blood-red fields within the United States and western Europe. This becomes apparent when you decide to compare ETFs tracking the Western economy with those tracking emerging ones, as the average P/E ratio of an S&P 500 ETF is close to 28.10, whilst EM ETFs hover around 19.62 (Oxford Business Group, 2021). The same comparisons as in Image also hold when comparing CAPE ratios, Price/Sales ratios, and Price/Book ratios (Strauss, 2020), which shows that there is more than one factor indicating possible undervaluation

Image 2: Global overview of fundamental valuation ratios.

Although there are risks involved due to the unpredictability and uncertainty of governmental and COVID-related developments within emerging markets, it remains a very tempting investment opportunity, nonetheless. Emerging markets are blossoming into economic powerhouses that are set to dominate the world stage for decades to come, and their growing consumer base promises increasing revenues for many years to come. Will this finally be a reversal for the fortunes of emerging markets?

Bibliography

Lazard Asset Management. (2021, January). Outlook on Emergin Markets . Retrieved from Lazard: https://www.morningstar.co.uk/uk/news/207580/emerging-markets-outlook-2021.aspx

Morgan Stanley. (2020, December 1). 2021 Global Economic Outlook : The next phase of the V. Retrieved from Morgan Stanley: https://www.morganstanley.com/ideas/global-economic-outlook-2021

Oxford Business Group. (2021). Guide to top emerging markets for 2021. Retrieved from Oxford Business Group: https://oxfordbusinessgroup.com/guide-top-emerging-markets-2021

Strauss, A. (2020, Nov 30). Why Now Could Be The Time To Look For Value In Emerging Markets. Retrieved from Pekin Hardy Strauss Wealth Management.

The Emerging Market Investor. (2021, January 14). Ten Years of Woe In Emerging Market Stocks. Retrieved from The Emerging Market Investor: https://www.theemergingmarketsinvestor.com/category/investing/

Umland, K. (2020, August 31). Ins and Outs of Emerging Markets Investing: Market Behavior and Evolution. Retrieved from Dimensional: https://www.dimensional.com/us-en/insights/ins-and-outs-of-emerging-markets-investing

Yahoo Finance . (2020, December 10). ECB: Eurozone economy set for slower COVID recovery. Retrieved from Yahoo Finance: https://uk.finance.yahoo.com/news/ecb-december-eurozone-economic-forecasts-policy-meeting-143826353.html#:~:text=The%20ECB%20now%20expects%20GDP,countries%20to%20return%20to%20lockdowns.