Amid international conflict, historic inflation rates and getting used to a post-pandemic world, the global chip shortage seems insignificant. If you can’t order a PlayStation 5, you simply wait until it’s available again or purchase a different gaming console. In that context, it seems like a minor inconvenience. Yet headlines continue to relay urgent messages regarding the chip shortage. So, what’s actually going on? And, more importantly, are there investment opportunities worth looking into?

The semi-conductor industry is a roller-coaster ride regarding the cyclical nature of its product. When technological advancements occur, demand heightens, and supply shortens. As soon as the technology is upstaged, demand crashes and supply goes unsold. The industry continuously strives to revolutionize its product, not even waiting for the dust to settle on its previous innovation. It is driven by worldwide economic growth (demand) and inventory (supply).

The corona-crisis exposed the extent of dependence that companies have on the supply-side of semi-conductors. The immense demand for technological products following pandemic legislation could not be fulfilled and led to a global chip shortage. This shortage remains a bottleneck for various industries to this day. Certain cars are unavailable, TVs and game consoles like the PlayStation 5.

The global chip shortage has put a spotlight on the semiconductor industry. It shed light on the fact that there are a few manufacturing companies monopolizing the market. This sparked governmental debates and countries announced they will increase their investments in the semi-conductor industry.

The current government involvement is in stark contrast to industry predictions. Three years ago, McKinsey (2019) expected that “well-established in-house manufacturing facilities, such as Intel, are considering partial outsourcing to chip foundries”. The prediction suggested that outsourcing would remain the norm, as companies may benefit from “greater production flexibility and cost reductions”. Three years later however, the pandemic spurred governmental involvement. Consequently, The U.S. President Joe Biden (2022) announced the $20 billion investment by Intel to build a semi-conductor factory in Ohio. This is an example of how the U.S.A. plans to further expand domestic chip manufacturing.

To elaborate, chip foundries are the semi-conductor manufacturers. The foundries have fabrication facilities, also known as “fabs”. The fabs create the hardware for the “fabless”. The value-adding players of the semi-conductor industry are the fabless, as they design and market the hardware. Fabless companies are for example Apple, Qualcomm and Nvidia.

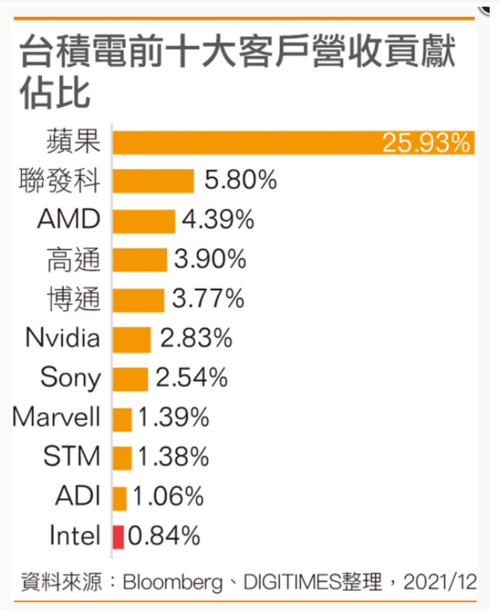

The fabless may be the value-adding players of the semi-conductor industry, but a close collaboration with a fab strengthens its position in the industry. It may even extend to advantages that prevent supply chain disruptions. This unique benefit is reflected in the ten-year partnership between Apple and its manufacturer, The Taiwan Semiconductor Manufacturing Company (TSMC). In December 2021, data from Bloomberg and Digitimes exposed that Apple is responsible for 25.93% of TSMC’s revenue.

It is unique how Apple works closely with TSMC early in the manufacturing process, to provide an optimal chip design (AppleInsider, 2021). The combined effort produces cutting-edge chips and TSMC has ensured capacity so Apple can continue to supply its products amid the global chip crisis.

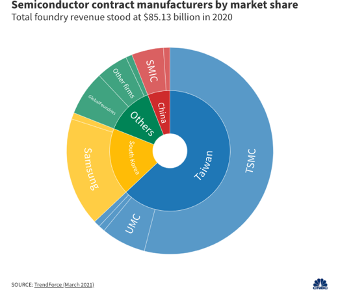

The pandemic exposed the vulnerability and dependence on the manufacturing companies. As a result, a newcomer to the foundry fray is Intel. It is geared up to benefit from governmental support and expand manufacturing countries in the U.S. Currently, the global leader with a 54% market share in the foundry sector is the previously mentioned TSMC.

Its closest competitor on the global market is Samsung, based in South Korea and holding a 17% share. In October 2021, it announced plans to “triple foundry production capacity by 2026”. The ambitious plans are reminiscent of its rival TSMC. The Taiwanese became the global industry leader by identifying market opportunities and seizing them accordingly. It profited from investor optimism during the dot-com bubble, as it was listed on the NYSE in 1997. Samsung’s announcement plays into the global chip shortage as well as governmental concern. A month after the initial announcement, Samsung confirmed it will build a semiconductor fabsite in Texas. However, Samsung itself is a competitor in the smartphone industry. This challenges the acquisition of fabless customers who may be a direct competitor.

The nuts and bolts within the industry are companies like ASML. It is unique to fabs, as it provides specific components needed for semi-conductor manufacturing. In the semi-conductor industry, ASML is considered as a provider of capital equipment. Globally, it is the only company that designs and manufactures lithography machines.

For investments in the semi-conductor industry, it is important to remember that the value-adding companies (fabless) are highly dependent on the stable partnerships in the first stages of the supply chain (fabs). Also, fabs are dependent on companies, like ASML, that provide crucial parts. The current market players play specific parts in the production process. Despite the industry’s size and importance, the geography of the industry remains undiversified. The pandemic exposed this vulnerability, resulting in governmental involvement. In a very optimistic outlook for the future, the involvement may lead to subsidies which could possibly soften the revenue blow when demand changes, decreasing the volatility of this industry.