In one of our previous in-depth articles, we mentioned how inflation could potentially impact your portfolio. In this article, we will look at an asset class that benefits from a prolonged period of inflation: real estate. Real estate is an asset class that has produced around 90% of millionaires over the past two centuries. As investing in real estate requires a lot of capital, this article will focus on REITs, which are more liquid and limit the capital requirement.

The history of REITs began in 1960 when president Eisenhower signed public law 86-779 into effect that gave investors the opportunity to invest in large-scale diversified real estate companies. In the US most of these real estate companies are referred to as REITs (real estate investment trusts), but do note that this is not the case everywhere. Initially, most REITs were mortgage REITs that grew by providing loans for construction and land development. However, the main focus of today’s article is equity real estate companies, companies that actually own the land and buildings.

As was established in one of our previous in-depth articles, we are currently seeing prolonged levels of high inflation. The effect of inflation on REITs has generally been positive. The reason for this is that most leases provide protection against inflation. Real estate companies that deal with short-term leases (such as Apartment REITs) are protected as these leases are based on current prices. Companies that deal with long-term leases usually have inflation protection built into their leases. As an example, VICI Properties, an owner of net lease casino and hotel real estate (such as the Venetian and Caesars Palace in Las Vegas), has the majority of its leases tied to CPI (pre-merger).

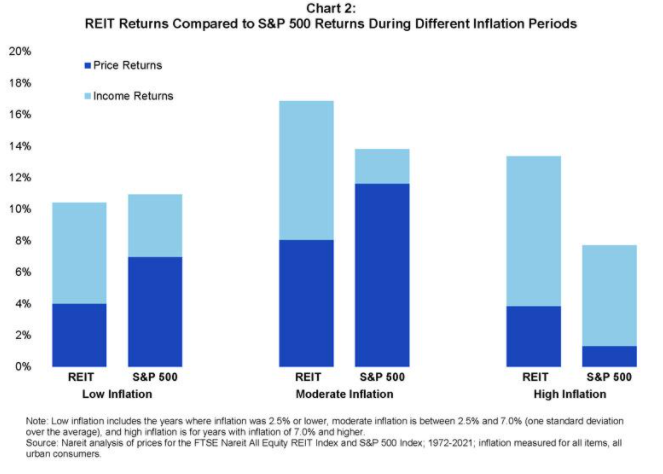

NAREIT, the REIT industry association, has done research on the performance of REITs in times of low, moderate, and high inflation. The only time that REITs underperform is in times of low inflation (inflation below 2.5%). The main reason for this is that the dividends make up for the lack of capital appreciation in times of moderate and high inflation.

Source: NAREIT

You might wonder what kind of real estate you can buy or think that real estate is boring and you just want to invest in tech companies. Fortunately, there are a lot of different types of real estate and all of them have different characteristics. It is important to take into account these differences and the effect they will have on the business. As an example, if you are into tech, you could invest in data center REITs or cell tower REITs, or if you think that the housing shortage will continue you could invest in apartment, single-family, or manufactured home REITs. To give you a general idea about the sectors that are available in the REIT/real estate world, you can take a look at the table below.

|

Sector |

Subsectors |

Main type of lease |

Fast Facts |

Companies examples |

|

Residential |

Apartment Manufactured Housing Single-Family Student housing |

Short-term |

Highly fragmented, Essential, Rent growth has outpaced inflation since 1995 |

AvalonBay Communities (NYSE:AVB) Equity Residential (NYSE:EQR) Vonovia (ETR:VNA) |

|

Retail |

Mall Strip Centers Outlet centers Shopping Centers |

Majority: Mid-term Anchors: Long-term |

Covid 19 has accelerated bankruptcies, In the US malls are overbuilt, Significant CAPEX, Work best in densely populated areas |

Simon Property Group (SPG) Unibail Rodamco Westfield (AMS:URW) Tanger Factory Outlet (NYSE:SKT) |

|

Office |

Office Laboratories Shared working space |

Long-term/short-term |

Higher CAPEX and lease free burden, Best performers have low cost of capital |

Alexandria Real Estate (NYSE:ARE) Boston Properties (NYSE:BXP) IWG PLC. (LON:IWG) |

|

Healthcare |

Skilled nursing homes Hospitals Medical office buildings (MOB) |

Skilled Nursing Homes: Short-term Hospitals: Long-term MOB: Long-term |

Large percentage of GDP goes to healthcare, Lot of people will reach retirement age in next 10 years (Silver Tsunami) |

Medical Properties Worlwide (NYSE: MPW), Omega Healthcare (NYSE:OHI) Physicians Realty Trust (NYSE:DOC) |

|

Self-storage |

Self-storage |

Short-term |

Increased housing prices leads to higher demand, 40% of renters stay longer than 24 months, Low CAPEX |

Public Storage (NYSE: PSA) Life Storage (NYSE:LSI) Shurgard (EBR:SHUR) |

|

Lodging |

Hotels |

Day-to-Day lease |

Hotel REITs own hotels operated by c-corps (Marriott, Hyatt), High capital intensity + low margin, Bad performance during recessions, |

Ryman Hospitality Properties (NYSE:RHP) Host Hotels and Resorts (NDAQ:HST) Apple Hospitality REIT (NYSE:APLE) |

|

Technology |

Cell Towers |

Long-term |

REITs own the majority of cell towers, Equipment upgrade and densification drive growth, High operating leverage + Tenant Switch Cost + Barries to entry |

American Tower Corporation (NYSE:AMT) Crown Castle Internatioanl (NYSE:CCI) Cellnex (BME:CLNX) |

|

Technology |

Data Centers |

Mid-term & Long-term |

IOT will lead to higher usage of data Energy costs can have a big impact on margins |

Digital Realty (NYSE:DLR) Equinix (NDAQ:EQIX) Iron Mountain (NYSE:IRM) |

|

Logistics |

Industrial Warehouses |

Long-term |

Demand fueled by Ecommerce and supply chain densification Limited supply of high value logistics centers Distribution and Last-mile are fastest growing segment. |

Prologis (NYSE:PLD), STAG Industrial (NYSE:STAG), Industrial Logistics Properties Trust (NDAQ:ILPT) |

|

Specialty |

Gaming Cannabis Billboard Farmland Prisons Timber |

Depends on the subsector |

Differs per subsector |

Innovative Industrial Properties (NYSE:IIPR), Farmland Partners (NYSE:FPI) Weyerhaeuser (NYSE:WY) |

Sources: Wide Moat Research, Yahoo Finance, NAREIT

In the overview that we provided we deliberately did not include net lease REITs, as these are a special kind of breed. The name net lease refers to the triple net lease structure, in which tenants are responsible for property maintenance, property tax, and property insurance. The reason why it was left out of the table is that it can be part of most of the sectors discussed above. For example, Realty Income (NYSE:O) owns retail real estate, while its spin-off Orion Office REIT (NYSE:ONL) owns office real estate. In the current economic environment, most net lease REITs will do well as their leases include an escalator, such as the consumer price index.

After deciding which subsector you want to invest in, it is time to value the company. However, it is important to keep in mind that this works slightly differently than for other publicly listed companies. A lot of people try to value real estate companies by using standard metrics such as a company’s PE ratio and a discounted cash flow calculator. I have bad news for them, it does not work. There are multiple reasons why it does not work and one of them is that commercial real estate increases in value over time and the acquisition of new properties will lead to an increase in revenue. Instead of using P/E, investors could use the P/FFO and P/AFFO. FFO stands for funds from operations and AFFO stands for adjusted funds from operations. FFO is similar to operating cash flow and AFFO is similar to recurring free cash flow. The basic computations for FFO and AFFO are the following:

FFO is equal to GAAP net income excluding the following items:

- Real estate depreciation and amortization

- Gains and losses from the sale of real estate

- Gains and losses from a change in control

- Impairment write-offs when they are directly attributable to the decrease in real estate.

As a formula, it would look like the following:

FFO = GAAP Net Income + Depreciation & Amortization – Gains from Property Sales or Change in Control + Impairments from Real Estate Depreciation

AFFO is similar to the aforementioned FFO with one adjustment. You have to subtract maintenance CAPEX. Therefore:

AFFO = FFO-Maintenance CAPEX

To give you a better understanding we will use an example of Prologis. The following screenshot has been taken from the company’s 10K:

Source: Prologis 10K

Analyzing Prologis is rather easy as it already provides you with the FFO as defined by NAREIT. However, the company also provides other ways of calculating its FFO. For an investor, it would be the easiest to use one formula as this makes it easier to compare companies. If we would like to know the company’s AFFO we would have to make the calculation ourselves as the company does not provide AFFO. To find the company’s maintenance CAPEX we will use the company’s cash flow statement. When we look at the company’s investing activities we see two lines that could be considered maintenance CAPEX: Tenant improvements and property improvements.

Source: Prologis 10K

Thus, to get AFFO, we subtract $329.059.000+$169.933.000=$498.992.000 from $3.924.000.000, which leaves us with an AFFO of $3.425.008.000.

To value Prologis we could use the company’s FFO and AFFO. As an example, we could use a comparable company’s analysis to compare the company’s AFFO and AFFO growth to competitors or we could discount the AFFO to make it similar to a discounted cash flow analysis.

Hopefully, by now you have a better understanding of how REITs work and are able to start analyzing them on your own, so that you can join the other millionaires that got rich in real estate.