The term metaverse was first coined by, as one would expect, a science fiction writer; Neal Stephenson. In the book, Snow Crash, the Metaverse is a virtual universe that exists next to the physical one, much like the one that is being created at the moment. In the book however, the Metaverse did not have a great connotation. In the book, most of the power is in the hands of a couple of immense companies. The real as well as the submersive reality is one of immense disparity and economic injustice. In the book there is an electronic virus that causes the metaverse users to have brain damage in the real world. For companies and especially a company under scrutiny for monopolistic tendencies you might not see this as a novel to base your name on but there you go. Now that the book report is over, let’s look at the real deal.

At the moment you have different companies trying to create meta worlds, the most popular of which are Decentraland and Sandbox.

Decentraland is one of the oldest, being around since 2015. Decentraland’s Genesis City is a virtual world about the size of Washington D.C. It looks as you would expect, with your avatar walking through the world created being built or already built by others and possibly, if you are fortunate enough, yourself. The auction of the fixed number of plots raised 28 million. The plots are being used for different endeavours, there is an equivalent of Las Vegas being built. There are also less recreational uses possible, Ripio.com, a crypto credit network bought a plot for 150.000 dollars which they are going to use for issuing and advising on mortgages on Genesis city plots. This purchase is nothing compared with the purchase of Tokens.com, who bought 6,090 square feet for a whopping 2.43 million dollars, this comes to a price of close to 400 dollars per square feet. The company said it would use the plot to develop the digital-fashion industry in the fashion street district where the plot is located.

Then there’s Sandbox. Their last investment round raised $93 million.The biggest investor was SoftBank which invested close to 30 million dollars. Although SoftBank has not been exactly Nostradamus in recent times, it is still a meaningful indication. They also collected 144 million dollars in NFT sales with over 12.000 unique “landowners”.

Every meta-world has their own currency with which they pay. The value of meta-world coins has skyrocketed ever since the announcement of Facebook changing their name to Meta.

In the meta world you can buy most of the same things that you can buy in the real world - clothes, games, etc. - you can even go to a concert. There have been a couple of experiments with this. On Fortnite there have been a couple of virtual concerts. Three years ago Travis Scott did a concert with Fortnite which was watched live by 12.3 million people and tens of millions more on social media afterwards. It is also profitable for the artist as Travis reportedly grossed close to 20 million dollars which included sales of physical as well as virtual merchandise, more popular known as skins. This while his global tour in the same year grossed 53.5 million dollars. For this he had to do 69 shows over 9 months while the Fortnite concert took a whole 10 minutes and wasn’t even live.

There are also exciting prospects for sports with Manchester City and Sony working on a metaverse version of their stadium which fans can visit and there are also people working towards virtual sports.

Digital currency investor Grayscale estimated that the revenue of goods and services in the global market of the metaverse will be worth 1 trillion dollars in the near to medium future.

Another buzz word in the latest year has been NFT’s, however there is still a lot of doubt as to the value of NFT’s and where it lies. One investor described their possible value as a pass to get into different worlds and clubs if you possess a certain NFT. This prediction is starting to ring true as the Bored Ape NFT, one of the most popular at the moment also doubles as a “Yacht Club membership card, and grants access to members-only benefits, the first of which is access to THE BATHROOM, a collaborative graffiti board. Future areas and perks can be unlocked by the community through roadmap activation.” If this sounds like nonsense gibberish to you; one of these 10.000 ‘limited edition’ NFT’s is going for 86.000 dollars on average at the moment, and growing.

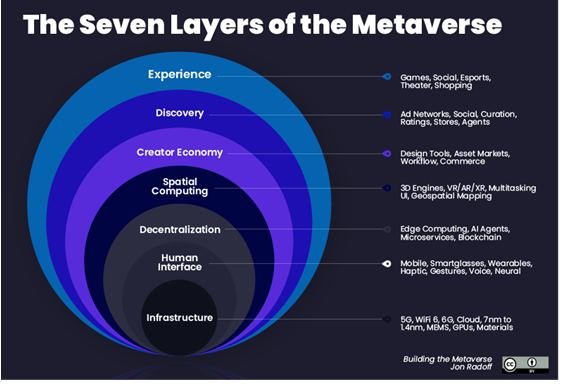

All of this is terribly exciting and it might very well be the future, but it is still a long ways away from completion or viability. Below you can see a picture that describes the layers of the Metaverse. Only the first layer is one that is currently viable for the real world, the other layers are being developed specifically for the Metaverse. If you look at the infrastructure, most of it is already there but it needs to be extended and innovated to be in the vicinity of where it needs to be. In the rest of this article we will go through the main infrastructure of what is needed to build the Metaverse but will not terribly diminish in value if it proves not to be the golden egg everyone is saying it is. We will make this the basis for a virtual picks and shovels META ETF to rival Meta ETF’s currently out there that aren’t hedging their bets.

As we stated in the title of the article, the current Web 3.0 hype is starting to look like the California gold rush of the 1850’s. One vital player in this gold rush was Sam Brannan. He was one of the first visitors of the newly discovered gold mines near Coloma in 1847. He left with a single vial of gold, yet his enterprising spirit led him to become California’s first millionaire. His success came from his unique approach to the gold rush. Instead of digging for gold, he bought the equipment needed to do so and sold it at a sharp mark-up. Consequently, he held the title for the richest man in California during the 1850s and 1860s.

With a little imagination, you can compare our hypothetical ETF in the metaverse to Sam Brannan’s approach. Looking past Mark Zuckerberg’s glitzy promotion video and digital concerts, the metaverse remains intangible and arguably vague. Prior to publicising their Q4 2021 earnings report, Meta warned that the investments took a chunk out of profits, as it needs time to engineer the third web. Instead of waiting for the end product to finalise, we analysed various investment opportunities regarding the hardware needed to create the metaverse.

Semiconductors

The demand for semiconductors has been an absolute given in the last decade with ever growing expertise and innovation at the forefront of the battle for more computing power. This will also develop into the Metaverse with Intel estimating that Web 3.0 metaverse projects will demand at least 1000 times the computing power they are currently capable of producing. The semiconductor industry will be a vital part of the infrastructure of the metaverse with a recent CNBC article stating: “It’s a natural and necessary part of tech’s maturation, and it keeps the semiconductor mainstays like Intel and Nvidia in a solid position, whatever becomes of the metaverse.”

The corona-crisis exposed the dependence that companies have on semiconductors. The immense demand for technological products on a short-term basis could not be fulfilled and led to a global chip shortage. This shortage is a bottleneck for various industries and led to the unavailability of certain cars, TVs and game consoles like the PlayStation 5. The global chip shortage has put a spotlight on the semiconductor industry. It shed light on the fact that there are a few manufacturing companies monopolising the market.

Governmental debates followed suit and countries announced an increase in investments in the semiconductor industry. For example, the U.S. President Joe Biden (2022) announced the $20 billion investment by Intel to build a semiconductor factory in Ohio. The recent announcement is an example of how the U.S.A. plans to further expand domestic chip manufacturing, if Congress passes the legislation.

Unsurprisingly, the semiconductor industry plays a crucial role in the metaverse. Manufacturing companies like The Taiwan Semiconductor Manufacturing Company, are preparing for a new role revolving around innovation. Ultimately, TSMC strives to create chips that make AR/VR products widely adoptable. Currently, TSMC is a global leader in the foundry sector and holds a 54% market share. It manufactures for Apple, whom is a promising prospect in the metaverse developments. The Wall Street Journal deemed that “consensus view is that the real catalyst for mass market AR/VR adoption will come when Apple enters the market”. With TSMC as a manufacturer that has been around since 1987, together with the products that Apple wants to create for Web 3.0, speculators think that their contributions will make the metaverse user-friendly and draw in consumers.

Another promising newcomer to the foundry fray is Intel. It is geared up to benefit from governmental support and expand manufacturing to the point that it reaches its ambitious plan to surpass TSMC and Samsung in 2025. To do so, Intel’s CEO Pat Gelsinger wants to increase Intel’s presence in chip manufacturing globally, by building chip fabrication facilities in the U.S., Europe and Israel.

Despite Intel’s ambition and TSMC’s history, the ultimate value-adding players of the semiconductor industry are the “fabless”, as they design and market the hardware. Fabless companies are for example the previously mentioned Apple, but also Qualcomm and Nvidia show strong presence for the metaverse. Nvidia is “a market leader in the design of graphics processing units”, an inevitable piece of the metaverse goal to make virtual reality as realistic as possible. Similarly for Qualcomm, another fabless player that concerns itself with the Oculus headsets from Meta. It strives to make the metaverse feel real through an immersive and wearable experience.

Digital infrastructure

Successfully realising the metaverse implies global access, such that everyone can benefit from this revolutionary phenomenon in this new information era. Consequently, providing stable, global and open access to the metaverse means a higher demand for ultra-fast internet connectivity. From a technical point of view, Metaverse has very high requirements for bandwidth, storage, and computing, which may be 10 levels higher than the requirements of the Internet era. This provides the opportunity to datacenter and telecom developers and operators to monetize on this demand, and make the required investments to meet this demand. One key investment, to meet this demand, is to deploy 5G networks, which will enable the required bandwidth, storage, and computing.

In August 2021, GSA confirmed the number of launched 5G networks stands at 176, with a presence in 72 countries. This figure is expected to grow as 461 operators in 137 countries/territories are currently investing in 5G, including trials, acquisition of licences, planning, network deployments, and launches. Mobile carriers invested billions of dollars into 5G networks which is why it is not surprising that they are betting on a futuristic concept that can give them a fair share of returns in time. GSMA Intelligence predicts $720 billion worth of spending on 5G networks between 2021-2025 globally.

In order for Telcos to provide these services to the population we will need cell towers. Telcos do not own all the cell towers themselves and the majority are actually owned by real estate investment trusts. This lowers the cost considerably as cell tower REITs can rent the space on the cell tower to multiple companies and thus lower cost. However, in order to reach the full speed of 5G we need a lot more cell towers than we currently have, as there is a huge difference between the way 4G and 5G work. The main difference is that 5G works with millimetre waves (mmWaves), which were largely untouched in 4G. The advantage of mmWaves is that these frequencies are less cluttered. However, this comes at a cost as it cannot travel the same distance as the current frequencies.

This growth does not mean that we will have huge cell towers at every street corner in the future. Nevertheless, it does mean that we need something to transmit the data. To do this we use antennas and small cells. Small cells are smaller low-powered access points of cellular data. There are a lot of different small cells and they can reach anywhere from 10 metres up to a few hundred metres. In general small cells will play a big role in 5G as it is an easier way to gain network densification. There is a disadvantage to small cells as it is harder to reach the same margins as you require a lot more small cells to reach the same amount of people, this leads to higher cost for site acquisition, installation and backhaul facility. Thus, it remains to be seen what the best way forward is for cell tower companies.

At the moment there are 6 main public cell tower companies who are in this atmosphere, of which 3 are from the US. All of them have implemented a different strategy. The 6 companies that are public are: American Tower Corporation (AMT), Crown Castle International (CCI), SBA Communications (SBAC), Telesites S.A.B. (BMV: SITESB-1), Indus Tower (NSE:Industower), and Cellnex (BME:Cellnex).

Another vital part of the digital infrastructure is the collocation ecosystem:

On February 10th 1960, The New York Times headed a story about Royal Dutch Shell being the first customer of IBM’s so-called data centre located on 1271 Avenue of the Americas (6th) in New York. The systems were used “to calculate the economics of the petroleum distillation method”. The calculations took 6 minutes to complete, 800 times faster compared to then using “manual computing techniques”' and what a great leap forward it was.

Now it is hard to imagine a datacenter in a block let alone an office on 6th avenue, with the largest data centre reaching over 10,5 million square feet. But even these aren’t sufficient. The infrastructure needed requires not only a big data centre, but it requires an integration of the infrastructure currently in place as well as an expansion of different factors within the current infrastructure. The workload placement consists of three main components, which are the traditional on-premises data centres as well as cloud, and edge providers. These will need to integrate to make for an effective digital infrastructure. In a recent report by Gartner, a major Connecticut-based technology research and consulting company, it was stated that “By 2025, 85% of infrastructure strategies will integrate on premises, colocation, cloud and edge delivery options compared with 20% in 2020.”

While the Big five do own their own datacentres around the globe and lead the charge in building some new datacentres, they also lease roughly 70% of their datacentre footprint from datacentres owned by other companies.

Besides the big players most all of the other possible participants make use of datacentres that aren’t operated by themselves. Super League Gaming (Nasdaq: SLGG) for instance, a big player in the world of video game experience and the gameplay content for the metaverse makes use of Equinix Metal and their datacentres.

The builders best prepared for the building of entire colocation ecosystem in line with the demands for the metaverse are Coresite, Cyxtera (NASDAQ:CYXT), Digital Realty (NYSE:DLR), EdgeConnex, Equinix (NASDAQ:EQIX), NTT Global (TYO:NTDTY).

A company that is involved in both telecom and data centres is AMT. The company has a market cap of $113.72 billion at the moment of writing and its towers are located all over the world. The company’s main focus remains large cell towers. However, on November 15th 2021 it announced that it would take over data centre REIT Coresite Realty for $170.00/share totaling 10.1 billion dollars. In this process of thinking enlies the synergies that they see in taking over Coresite and these two industries being the cornerstone of the digital infrastructure.

Crypto

We already have defined the metaverse and its relation with physical infrastructure, but what about the impact of cryptocurrencies on its development? Here, we will seek to determine the impact that cryptocurrencies have on virtual worlds and how we could extract value from this connection without taking too much risk. Indeed, our philosophy here is still to find bets on the metaverse that bring great upsides and very limited downsides.

The particularity of the metaverse is that the user is entirely immersed in the experience and life he has inside the virtual world, hence the use of cryptocurrencies has been widely adopted inside every already created metaverse. One of the benefits of cryptocurrencies for metaverses is the blockchain technology, the public ledger allows for the creation of proof of ownership. This proof permits users to own things inside the virtual world, the ownership can be of anything, ranging from virtual real estate to objects in the metaverse such as pictures, avatars or collectables.

Some blockchains offer the possibility of creating a “smart contract”, like ethereum for example, these contracts are routines created on the blockchain that will run once a condition is met. Effectively, this is what grants the proof of ownership and allows for the transmission of digital assets without the involvement of a third-party, such as a bank or in our case companies like facebook. To be usable, the assets must be recorded on a widely adopted blockchain. It is important to understand that the future of the metaverse is strongly linked to blockchain technology.

To conclude, if metaverse technology develops and becomes adopted across the population, blockchain technologies will also grow in popularity and might appear as interesting investments. However, we are only at the beginning of the trend and even if the three currently bigger metaverses are all built on the ethereum blockchain, it might change later in the future. As new blockchains are created at an increasing rate and might replace the ones considered as market leaders. Blockchains offer many applications, the technology is not dependent on the deployment of metaverses. Finally, the world of digital/crypto assets is an extremely volatile market, repelling risk-averse investors, so investing in individual blockchains is too risky for most investors.

Hence, ETFs focusing on blockchain tech might be more interesting for investors looking for a safer exposure. Funds following digital assets: Greyscale or ETF following firms exposed to the adoption of the blockchain technology, such as : Amplify Transformational Data Sharing ETF (NYSEMKT:BLOK) or Reality Shares Nasdaq NextGen Economy ETF (NASDAQ:BLCN) are very interesting products.

Building the ETF

Two ETFs focused on the metaverse opened in 2022, they currently are the two biggest fund regarding investment in the metaverse: METV - METV | Ball Metaverse ETF - Roundhill Investments and PUNK PUNK Subversive Metaverse ETF.

We want investment opportunities with high upside if the metaverse takes off and small downside if it is not adopted by the public. To create this ETF, we will go over each industry that we covered so far, and pick interesting stocks that could constitute an ETF following our strategy. In this part we will discuss the biggest weights as well as the, in our opinion, most interesting ones.

For the Semiconductors weight of the portfolio we put more weight into the fabless companies which are more expertised towards the Metaverse, these are Apple (NASDAQ: AAPL), Nvidia (NASDAQ NVDA), Qualcomm (NASDAQ: QCOM). Besides that we also focus on the Fab companies where we put weight in TSMC (TPE: 2330) and Intel (NASDAQ: INTC)

When discussing the digital infrastructure we look at the companies most in line to produce this infrastructure. We already touched on it in the piece but the companies most involved in building this infrastructure are: Digital Realty (NYSE:DLR), Equinix (NASDAQ:EQIX), , American Tower Corporation (NYSE: AMT), Crown Castle International (NYSE: CCI) and SBA Communications (NASDAQ: SBAC)

Concerning the crypto-related industry, the safest bet is to invest in blockchain technology. To do so, we look at the two main blockchain ETFs, BLOK and BLCN, and check which stocks are included in both ETFs. From this curated list of seven companies, we will select the few that make the most sense regarding our strategy.

First, from the companies in two ETFs, the biggest mutual position is IBM (NYSE:IBM). For good reasons, as IBM is currently the largest blockchain services provider. The company has been patenting products related to the Blockchain and the metaverse for ten years. In particular, the IBM blockchain platform is used by massive clients such as Visa or HSBC and offers many applications. If in the future one private metaverse emerges as the leader, we can expect that his technology might be provided by IBM. The company is not dependent on its Blockchain division, hence offers exposure to the industry without taking too much risk.

Then, we look at Accenture (NYSE:ACN), the IT and consulting services company that now offers blockchain services. Through these services, consultants will help companies implement and understand blockchain technology to help the client develop their potential using blockchain tech. As Accenture is the leader in blockchain services, we believe the company allows for enough exposure to the blockchain to be in our ETF and offers enough diversified services to not be dependent on its blockchain services.

Finally, the last company we believe we should focus on is Coinbase (NASDAQ:COIN). Coinbase is the largest American cryptocurrency exchange platform. If the metaverse becomes widely adopted, a lot of payment will need to be done online, most of which will be made in cryptocurrencies. Moreover, as metaverses are built on specific blockchains, the cryptocurrencies related to these blockchain will gain in popularity and investing in the exchange rather than individual currencies is a safer choice.

We decided to add a small exposure to cryptocurrency in our ETF, this allows us to profit from the possibility that a specific metaverse gets widespread use in the future. For this reason, we decided to allocate money to the two current major metaverses: Sandbox and Decentraland. The cryptocurrencies SAND and TLM are used in play-to-earn metaverses where players can get them by creating art, leasing, or selling items. MANA is the cryptocurrency used in Decentraland to fuel the economy of the metaverse.

A possible next step for the metaverse is the “Petaverse”: one where your furry friend can join you. Recent developments intertwine high-tech blockchain technology with popular games from the early 2000s. Think of the Nintendogs of the future. The advancements are happening in a context labeled as “Petaverse”. It invites metaverse players to adopt dogs and maintain ownership through NFTs. One of the investors bringing seed money into DOGAMÍ, where you can adopt and raise a 3D dog, is Ubisoft. Together with Animoca Brands and The Sandbox, they invested a total of $6 million in the development of pet ownership 3.0.

Looking Glass Labs (NEO: NFTX) is a company that only recently went public on the NEO exchange. The company’s main focus is Non-Fungible Tokens (NFTs). The company can be split into 5 segments:

Overload: a play to earn NFT card game, where users can earn NFTs by participating

Project Origin: the company’s metaverse environment and digital distribution segment, where artists and players can create, play with and learn about NFTs

House of Kibaa: the digital studio that allows functional art and collectibles to exist in multiple metaverses/NFT environment

HOK utility token: the token that is used as the currency for all of LGL’s platforms

Virtual Asset Portfolio: a portfolio of perpetual royalty streams by, among other things, owning and selling NFTs.

The last security we want to highlight is ImagineAR.

ImagineAR is an Augmented Reality-Service self-publishing platform that allows users to integrate existing mobile phone apps to instantly create AR campaigns with no programming or technology experience. As the Metaverse becomes a key driver of new business opportunities, ImagineAR is positioned to deliver global immersive AR mobile engagements for businesses and consumers. Their latest product is FameDays.com, which is a metaverse hologram e-greeting platform. Using the FameDays mobile app, fans can enjoy life-size hologram video messages right in their home. Fans can record their own videos and pictures with the virtual star as if they are standing right next to them in real life and then instantly share the content via social media

Below we added our full ETF, you can use this as a concept to make your own depending on the level of direct exposure to the Metaverse.

https://docs.google.com/spreadsheets/d/1oOUSZD7A6T44qFaRKSDCJOvYMlYgClZN78HdGUbbTRo/edit?usp=sharing